For small businesses, late payments can have a serious impact on cash flow. With business to business transactions where no terms have been agreed or you do not have a contractual provision for late payment, the Late Payment of Commercial Debts (Interest) Act 1998 can step in to imply late payment terms into your contracts.

This means you may be entitled to charge interest on late payments, seek compensation on overdue invoices, together with reasonable legal costs. This helps businesses to recover losses caused by late payment and encourage prompt payments. Here’s what you need to know:

Statutory Late Payment Charges

Under the Late Payment of Commercial Debts (Interest) Act 1998 (“the Late Payment Act”), where applicable, businesses can charge the following:

Interest on Late Payments

Under the Late Payment Act you are entitled to seek:

- 8% per annum above the Bank of England base rate; and

- Interest can be applied daily from the date the invoice became due until the date payment is received.

Compensation

In addition to interest, you can also claim a fixed sum of compensation for each invoice, as follows:

- £40 for debts up to £999.99

- £70 for debts between £1,000 – £9,999.99

- £100 for debts of £10,000+

Recovery Of Reasonable Costs

You are also entitled to seek to recover an additional sum towards your reasonable costs if where the interest and compensation under the Late Payment Act do not cover all of your expenses in recovering the debt. Such expenses would include legal fees, debt collection agency charges or administrative costs.

How Lovetts Solicitors Can Help

At Lovetts Solicitors, we specialise in commercial debt recovery, helping small businesses:

- Sending Letters Before Action which can include interest and compensation under the Late Payment Act;

- Issuing legal proceedings to recover the debt, together with interest, compensation and reasonable costs if payment is not received; and

- Enforcing judgments obtained against debtors.

Late payments should never be accepted as the cost of doing business. If you are struggling with overdue invoices, take action today.

Dealing with overdue invoices can be a frustrating experience. However, there are effective steps you can take to tackle this common issue. In this blog post, we’ll explore essential strategies that will help your business collect late payments and maintain a healthy cash flow.

Understanding the Importance of Collecting Overdue Invoices

Late payments can disrupt the financial stability of your business, affecting your ability to pay suppliers and meet expenses on time. Unpaid invoices not only strain cash flow but also consume valuable time and resources that could be better utilised elsewhere. By promptly addressing overdue invoices, you demonstrate the importance of timely payment to clients and maintain a healthy relationship with them.

Step 1: Communicate Clearly and Early

When it comes to dealing with late payments and overdue invoices, clear communication is key for businesses. The first step in addressing this issue is to communicate openly and early with your clients or customers.

Initiate a friendly reminder about the outstanding payment as soon as it becomes overdue. Be polite but firm in your message, clearly stating the amount owed and the due date.

Utilise various communication channels such as emails, phone calls, or even face-to-face meetings if necessary. By being proactive in your approach, you can show that you are serious about collecting the overdue invoice while maintaining a professional relationship with your client.

Clearly outlining the consequences of non-payment can also serve as a motivator for prompt settlement.

Step 2: Set up a Payment Plan

Setting up a payment plan can be a proactive approach to facilitate the recovery process. By offering flexibility in how the debt can be repaid, businesses demonstrate understanding while also ensuring you receive what is owed to your business.

A well-structured payment plan should outline clear terms and deadlines for repayments. This clarity helps both parties stay on track and avoids any confusion or misunderstandings along the way. It’s essential to communicate openly about expectations and make sure all terms are agreed upon by both parties involved.

Step 3: Consider Legal Action

Sometimes the case may require more serious measures. This is where considering legal action can be a necessary step for UK businesses.

Legal action involves taking formal steps to recover the debt owed to your business through the court system. It sends a clear message to the debtor that you are serious about collecting what is rightfully due.

Before pursuing legal action, it’s important to review all documentation related to the debt and seek advice from debt recovery solicitors. We can provide guidance on the best course of action based on your specific circumstances.

Step 4: Utilise Debt Collection Services

By partnering with reputable debt recovery solicitors, you can increase the chances of recovering the money owed to you while maintaining professional relationships with your clients. As professionals we understand the legal aspects of debt recovery and can navigate complex situations efficiently.

Timely action is crucial when dealing with late payments and overdue invoices. Implementing these essential steps in your collection process will not only help you recover what is rightfully yours but also ensure smoother cash flow management for your business. Stay proactive, communicate clearly, consider payment plans, explore legal options if necessary, and leverage debt collection services to maximise your chances of successful debt recovery in the UK market.

If you’re unsure if your business debt is worth pursuing, check out our recent article here.

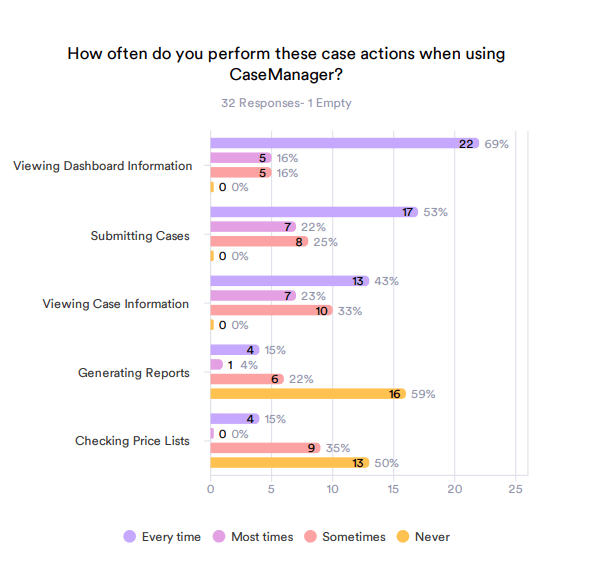

Lovetts online client portal, CaseManager is a unique case management portal which allows a client to have complete control over the debt recovery process. CaseManager allows clients to instruct Lovetts Solicitors and view their cases 24/7. To ensure CaseManager remains a market leading client portal for debt recovery, Lovetts is continually looking to enhance and develop it. Accordingly, Lovetts recently sent out a client satisfaction survey in order to gather our clients valuable feedback.

The results of the survey are detailed below and the feedback will enable Lovetts to provide our clients with the features and updates that they want to see. At Lovetts we want to make the debt recovery process as simple and stress free as possible. Accordingly 60% of clients that took part in the survey rated CaseManager’s ease of use either 4 or 5 stars out of 5.

66% of clients said they check case information either every time or most times that they login to CaseManager. With the remaining 33% saying they sometimes check case information. For us, this shows that this functionality is really useful and is time effective for both the client and for Lovetts as clients can simply login to their account and have their case information within seconds.

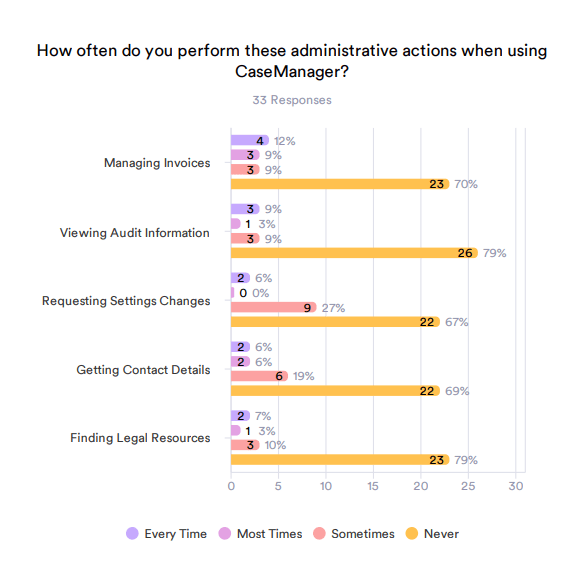

On the flip side we can see that 79% of clients that took part in the survey said that they never view auditing information or search for legal resources. Therefore this is something that we may look to remove.

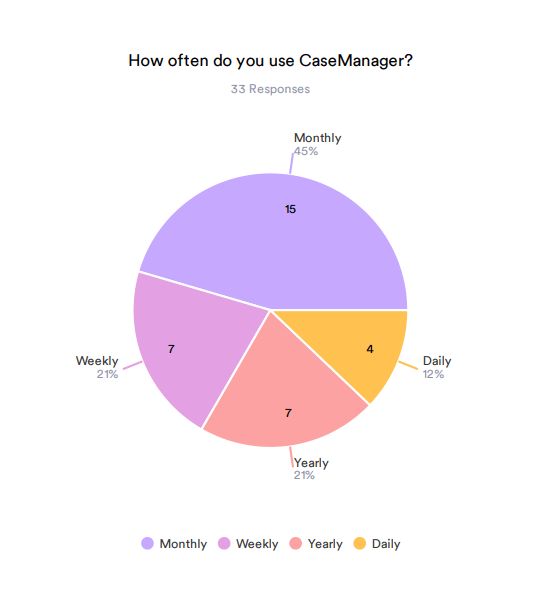

Most of our clients (75%) told us that they use CaseManager either daily, weekly or monthly with the remaining 25% using CaseManager yearly. CaseManager is so useful for many different reasons, not just instructing us on a case. Clients are able to check the status of cases, run reports, make changes/updates to their account and much more on CaseManager at any point in the day. Therefore, this result is assuring to see as we can imply that the information provided on their is useful for clients.

We would like to say a huge thank you to all of the clients that took part in our survey and allowed us to gather some valuable information which can be used to improve your CaseManager experience.

For every survey completed, Lovetts donated £2 to Oakleaf, which is a mental health charity Lovetts supports. They carry out fantastic work and Lovetts would like to thank all the clients that participated in the survey.

If you have any questions above the above please do not hesitate to contact us at [email protected]

ABN Amro Bank v RSA and Others (Court of Appeal, 2021)

One of the less attractive features of insurance from the policyholder’s point of view is that, when it comes to making a claim, insurers can raise the defence of misrepresentation of the risk or breach of a ‘warranty’.

However, it is possible, when buying insurance, to gain greater protection against claims being declined, by inserting a so-called non-avoidance clause (‘NAC’) into the terms and conditions of cover. When the insurance market is soft (i.e. hungry for business), this may not be expensive to obtain.

Duties on the purchaser of insurance – To explain, the law used to be that an insurance was a contract of utmost good faith, which insurers could avoid (i.e. rescind the contract) on the grounds of non-disclosure or misrepresentation of any matter material to the underwriter’s evaluation of the risk. Meanwhile, a breach of a warranty either suspended or actually terminated cover.

Consumer insurance – In recent years, certain protections have been introduced by statute. Thus, individuals who buy insurance for purposes mainly unrelated to their business now have the benefit of the Consumer Insurance (Disclosure and Representations) Act 2012. Put very broadly, in the area of providing information to the insurer this Act modifies the law such that the consumer’s duty is to take reasonable care not to make a misrepresentation (for example, when completing a proposal form) before the contract is entered into or varied.

Non-consumer insurance – Other types of insured, i.e. those taking out commercial non-consumer policies, have the benefit of the Insurance Act 2015 (which covers consumer insurance as well). For both types of insureds, the characterisation of utmost good faith has been removed. However, and again put very broadly, here the pre-contractual duty to provide information is re-cast as a duty of fair presentation, requiring the insured to disclose every material circumstance which the insured knows or ought to know; failing that, the insurer must be provided with sufficient information to put a prudent insurer on notice that it needs to make further enquiry for the purpose of revealing those material circumstances.

Although the legislation is intended to ensure a better balance of interests between policyholders and insurers, the provisions in the 2015 Act specifying what an insured is taken to know, or ought to know in the sense of what should have been revealed by a reasonable search of information available to the insured, could provide insurers with a basis for declining a claim. It may not be easy for an insured to be confident that a reasonable search of available information has been made, as such a search could involve having to seek information from employees or third parties and an evaluation of what circumstances are material in the context of the proposed insurance.

Under both statutory regimes, new remedies are available to the insurer in the event of the insured’s breach of duty, such as a lower level of indemnity or amended terms of cover.

Non-avoidance clauses (‘NAC’s) – Given these potential difficulties, various forms of clause have been developed for policyholders to insert into the insurance, to the effect that insurers will not seek to avoid, or seek damages, for non-disclosure or misrepresentation or to rely on breach of warranty, this being subject to a proviso permitting insurers to use their remedies in the case of deliberate or fraudulent misrepresentation or non-disclosure.

Such clauses are effective in accordance with their terms. However, they are in the nature of exclusion clauses. Accordingly they will be construed strictly against those they protect.

In particular, in order to be effective under judicial scrutiny, the drafting of such clauses needs to match the statutory regime now operating. For example, it may be prudent to provide specifically in a NAC that insurers will not decline cover on the grounds of (a non-fraudulent) failure to undertake a reasonable search of available information. Also, to provide that insurers’ waiver includes all of the various alternative remedies now available to them and not just avoidance.

Cases on non-avoidance clauses

The caselaw is building up to clarify the meaning and effect of NACs. For example,

- A NAC which at best contained the insurer’s general agreement not to raise ‘defences’ (but not referring specifically to breach of warranty) was insufficient, given the terms of the NAC as a whole, to prevent insurers from relying on breach of a warranty (HIH v New Hampshire (2001, Ct of Appeal).

- The proviso to the NAC, whereby the insurer was not bound by the NAC in the event of the insured’s own deliberate or fraudulent non-disclosure could, in the context of the policy as a whole, only be relied upon by the insurer in the case of a deliberate decision not to disclose a matter which the insured knew should be disclosed: the term ‘deliberate’ did not permit the insurer to rely on the proviso in the case of a merely honest mistake by the insured (Mutual Energy v Starr (2016, TCC).

- A broker informed two following underwriters that the renewal of an insurance was ‘as expiry’. In fact, because these underwriters had not been shown or agreed an endorsement adding certain additional clauses during the previous year of the cover, the renewal was not as expiring insofar as these two underwriters were concerned. When a claim was made under the additional clauses, the two underwriters argued that the insured was estopped from relying on the clauses because the broker had acquiesced in the underwriters’ understanding that the cover was as expiring. However, the court held that the brokers had simply made a misrepresentation as to the terms of the renewal. The two underwriters could not rely on this as a defence to a claim because the NAC in the policy was not confined to the remedy of avoidance but also prevented them from seeking to ‘reject a claim’ for loss on the grounds of misrepresentation, which words covered an argument based on estoppel by representation (ABN Amro v RSA and Others (2021 Ct of Appeal).

Lovetts’ comment

This note is intended to provide guidance of a practical nature but should not be taken as containing legal advice or any recommendation as to any course of action.

However, Wendy Miles, Chris Earl and William Sturge will be pleased to provide such advice should you require assistance in drafting any specific policy wording.

The use of mediation has grown significantly in recent years. Any party facing the prospect of, or already involved in, legal proceedings and who is willing to contemplate settlement will nowadays wish to consider mediation as part of the process of resolving the dispute. Other possible options may include simply making a Without Prejudice offer of settlement, lodging a claim via the Financial Ombudsman Service prior to proceedings, appointing an expert to make a non-binding appraisal, a judicial appraisal or, in the small claims track, a dispute resolution hearing conducted by a judge.

Features of mediation – Court proceedings, arbitration proceedings and expert determinations result in binding decisions (subject to the ability to appeal them). Mediation is not an alternative to these in the sense of inevitably producing a binding decision, but rather a voluntary process worth considering prior to or during the course of the formal proceedings. The crucial point is that mediation can prompt settlement where settlement might only be achieved much later, or not at all.

Advantages – Advantages of the mediation process can include speeding up resolution of the dispute, bringing all the parties who should be involved into a single set of negotiations, saving cost, confidentiality, a greater role and more control for the parties themselves, a more equal environment for the discussion of issues, preservation of relationships and solutions that benefit all parties.

Standard requirement to consider mediation – The Rules of Civil Procedure now require the parties to proceedings not to refuse alternative dispute resolution unreasonably, with possible adverse costs consequences if they fail to act reasonably in relation to the process. Accordingly, it should no longer be regarded as a sign of weakness for a party to propose mediation.

The process – Prior to the day of the mediation, a mediator will usually be appointed jointly by the parties. The parties and the mediator then usually enter into an agreement providing that communications in the course of the mediation will be Without Prejudice and therefore protected from being referred to in the proceedings if these have to continue because the matter cannot be resolved at the mediation.

The issues in dispute will usually be defined in the parties’ Mediation Statements, and a set of the key documents compiled. The mediator will read the documents and usually discusses the dispute separately with each party, in confidence. The mediator also clarifies with the parties who exactly will be attending the mediation.

On the mediation day, a representative authorised to settle must be available on behalf of each party. Representatives of each party will also usually be in the same building, in different rooms. The mediator presides over any plenary meetings of the parties and holds confidential discussions with each of the parties in turn, the objective being to identify the real issues of disagreement and the points that are most important to the parties. The mediator seeks to achieve agreement by carrying between the parties such messages as he or she is authorised to convey.

Mediators can suggest solutions to the parties but cannot impose one. It is simply a question of whether the mediator can bring the parties to agree between themselves.

The parties may or may not prefer to have their legal advisers present. However, it may be advantageous to have a legal adviser available to record the terms of any settlement agreement reached, to be signed before the parties disperse.

Choice of mediator – The choice of mediator is important for achieving a successful outcome. A number of organisations have grown up to provide training and accreditation, for example the Centre for Effective Dispute Resolution (CEDR). The mediator must be trusted by each party to do the job properly, for example, by acting impartially and saying no more to the other side about a party’s position than they have been authorised to say. The mediator needs to be a good communicator and it will assist hugely if each party believes that the mediator can provide an accurate assessment of the prospects of their case. Thus it is likely to assist if the mediator is a qualified professional, for example, a barrister specialising in the area of law in dispute, a chartered surveyor, or a qualified accountant, depending on the subject-matter of the dispute.

Mediation strategies – The flexibility of the mediation process is one of its strengths. For example, in one case, settlement may be facilitated by a plenary session of all parties at the start of the day, at which a party might apologise for what the other has suffered. Alternatively, the purpose of a plenary session might be to confront a recalcitrant defendant, albeit that an overly aggressive stance can set back the prospect of settlement and it may not be advantageous to be represented by counsel at a mediation. In another case, it may facilitate settlement for the parties not to set eyes on each other until a settlement can be reached. Logjams in the discussions might be eased by the mediator suggesting that just the parties’ professional advisers break out for a discussion, or just the decision-makers from each side. The timing for a proposal to mediate is also important. Too early, and the issues may not be sufficiently clear. Too late, and the costs already incurred may have become a barrier to settlement.

A party can withdraw from a mediation at any time. Parties often use the threat of departure to move along the negotiations. Even if the parties do not settle on the day, they often settle shortly afterwards, because they appreciate more vividly any difficulties with their own case and what would be involved in terms of time, effort, depth of investigation and expense in pursuing the proceedings to a conclusion.

Government schemes to reduce the cost of mediation – Various schemes operate to reduce the cost of mediation. If the dispute is over a money claim for less than £10,000, it may be possible to use the government’s free small claims mediation service (where the procedure may be slightly different to that described above). There is also a free rental mediation service for house possession cases. For claims under £50,000 in value, the Civil Mediation Council hosts a fixed fee mediation scheme.

Lovetts’ comment

It is worth considering mediation as it may be a quicker, cheaper and more controllable process than formal proceedings. It would only be in specific cases, such as where a party is seeking an injunction, or to establish their rights, or considers that there is no genuine dispute, that mediation may not be appropriate.

When drafting commercial agreements, it may be worth including a provision requiring the parties to consider mediation prior to submitting a claim to court proceedings or arbitration.

For more information, please contact Wendy Miles, Chris Earl or William Sturge at Lovetts.

About the Author

The author of this article is William Sturge a Consultant Solicitor at Lovetts Solicitors. William is a leading lawyer in the insurance industry. He has advised on insurance and reinsurance claims on behalf of reinsurers, reinsureds and their insureds, both in the UK and worldwide. He has conducted insurance and reinsurance litigation and arbitration, acted in professional indemnity and financial lines business and in shipping and international trade disputes. William has also provided non-contentious insurance and reinsurance advice, usually with an international context.

For further information or advice please feel free to contact William by emailing [email protected] or calling 01483 457500.

Lovetts, the commercial debt recovery law firm based near Guildford has appointed Michael Higgins as Managing Director, with immediate effect.

Michael joined Lovetts in 2007 and has played a significant role in its growth and the launch of innovative solutions to support the cost-effective and speedy recovery of bad debt. Michael, a qualified solicitor, joined the Lovetts management team in 2012, with responsibility for the Commercial Litigation Department and in 2014 he was made Operations Director. Michael will continue to report to Charles Wilson, the continuing Chairman of Lovetts who has, for the past 20 years acted as both MD and Chairman of the business.

Charles Wilson says “Michael has the right leadership qualities, client focus and legal expertise to take Lovetts from strength to strength. With some years of paralegal practice prior to professional qualification, he has the passion and determination to grow our reputation for innovation, thought leadership and superb customer service. We are delighted he has accepted the role of Managing Director and I look forward to continuing to work closely with him as Chairman.

Michael Higgins adds, “This role offers a fantastic opportunity for me to help shape our business, working alongside Charles and the rest of the team to ensure we not only deliver great products and services, but that we take responsibility for helping businesses understand their legal rights and the ways they can reduce their overall exposure to commercial bad debt. This is an exciting time for the business as we push ahead with our Claim the Unclaimed campaign and promote our newly-launched email LBA service, giving our customers cost-effective solutions to recover the money owed to them.”

Time From Invoice To Letter Before Action Increases 24% Year On Year

New figures on the amount of debt UK businesses are dealing with through late payment of their invoices throw into sharp relief the huge scale of the issue. With respected industry bodies such as The FSB and IoD calling for action, the new figures from Lovetts, the commercial debt recovery law firm, reveal suppliers are bank rolling their customers for an average of 103 days from the point they issue an invoice, before they threaten legal action with a Letter Before Action (LBA). This is a 24% increase on the amount of time the same sample waited in Q1 2014 when the time from invoice to LBA was 83 days.

From our figures, the scale of the late payment scandal in the UK is getting worse not better, despite the high profile campaigns to stamp out the problem. As the business climate improves, it seems that British businesses are reluctant to rock delicate client relationships by threatening legal action but their invoices will simply end up at the bottom of the pile. It’s vital that businesses act early on overdue invoices rather than delay. They also need to claim their right to compensation – not just for current customers but past customers who paid late too. It’s the only way the battle against habitual late payers can be won.

The Late Payment act allows any business paid late to claim interest for the period the debt was overdue, plus compensation. The entitlement to claim interest and compensation remains for six years on each and every invoice paid late, unless clear assent is proven against the claimant.

A growing number of businesses are now utilising the act to take on late payers, past and present and recovering significant sums to compensate them for the administrative and legal costs they have incurred chasing late payment. We want more companies to take action in this way – it will send a very clear message to late payers that delaying payment to their suppliers can seriously damage their bottom line.

This case study shows how by using the Claim the Unclaimed service provided by Lovetts, which uses the Late Payment of Commercial Debts (Interest) Act 1998 to recover historic interest and compensation, one client was able to recover over £41,000 in interest and compensation on past late paid invoices over the last six years.

Our client, a provider of physiotherapy services to a variety of medical and rehabilitation service providers faced a constant problem of their invoices repeatedly being paid late. This caused cash flow issues and meant staff had to spend a significant amount of time and effort chasing their customers for payment. Eventually in a number of cases our client had to cease working with their customer due to their persistent poor payment practices.

The Solution

Many businesses are aware of the Late Payment Act, which allows creditors to claim interest and compensation on invoices which are not paid to terms. However few businesses are aware that the legislation applies retrospectively, allowing claims to be made for any invoice paid late in the past six years (five years in Scotland).

Our client simply had to send a spreadsheet with a list of invoices paid late and Lovetts calculated the compensation and interest due.

Lovetts then wrote to the client’s past debtors to inform them of their ongoing requirement to pay statutory compensation for the past late paid invoices under the Late Payment legislation and request immediate payment.

The Benefit

Our client has now received payment of over £41,000 by claiming interest and compensation in number of cases. In 90% of cases this was achieved without the need to resort to legal action. Furthermore all new customers are now clearly warned on every invoice paid late will result in compensation and interest becoming due and that the only way to avoid this is to pay on time.

What Was The Cost?

The client used the services of Lovetts UK prelegal team who operate on a no collection no fee basis meaning there was virtually no risk to the client. Payment was taken as a percentage of any interest or compensation successfully collected for the client.

Find Out More?

Do you have past clients who were persistent late payers? If so then you could be entitled to significant sums under the Late Payment Act. Speak to us today and we can help you analyse your purchase ledger to see what you may be entitled to claim. And in most cases we will be able to do this on a no collection, no fee commission basis, meaning it won’t cost you a penny win or lose!

Beware! You can only claim interest and compensation if your Terms of Business allow for this. Don’t lose out – read our handy guide on the pitfalls of poorly drafted Terms of Business and make sure you aren’t making the same mistakes.

Costs recovery clauses to assure a cost free

debt collection service

Lovetts Plc, the commercial debt recovery law firm has seen a marked increase in businesses seeking its help to recover debts from the Middle East.

Middle Eastern debtors operate on the basis that if there is no signed contract then invoices will be rejected for payment. Many debtors in the Middle East are now using this as an opportunity to avoid payment to UK suppliers.However, unknown to many UK Companies, Middle Eastern debtors can prepare a summary paper outlining all events, for a bid committee to consider. The bid committee, which includes Government Ministers, approves payments when no contract is present by signing the summary paper.

The key factor in obtaining their approval is that there must be sufficient evidence to show that terms of business have been incorporated as if a contract was present.

While this process should ultimately result in payment, the process can be time consuming, adding months and sometimes years to the waiting time for payment to be made.

In a recent case handled by Lovetts, the UK firm had no signed agreement with a company in Egypt, and had been trying in vain for 3 years to recover the debt before approaching the pre-legal overseas team at Lovetts for help.

Lovetts established contact with senior personnel at the firm in Egypt and provided a paper trail to show the debt was due. A bid committee was requested for the case to be heard which subsequently approved the debt and payment was secured of over £40,000 on a no collection no fee basis.

Michael Higgins, Operations Director at Lovetts says: “The way Middle Eastern debtors operate has caught many UK firms unawares. It is imperative that businesses exporting goods and services to the Middle East, ensure they have a contract drawn up that is signed by both parties. Seek the help of your legal team or debt recovery experts with experience in overseas debt to ensure the contract is watertight. It’s vital that contract laws such as this do not become a barrier to overseas trade.”

Businesses face massive increase in cost of recovering debt, in Government ‘own goal’

This week, the Government has confirmed the implementation of its planned increase in Court Fees following a consultation process at the start of the year. With just 4 week’s notice, many businesses will face a 97% hike in the cost of pursuing over half of their claims for commercial debt. Lovetts, the commercial debt recovery solicitors is warning that increasing fees for debts between £1500 and £15,000 will damage the cashflow of small and medium sized firms in the midst of recovery, citing the move as a spectacular ‘own goal’ for the Government. As part of a set of measures to increase revenue from the Courts from £490m to £625m, Court Fees for small commercial claims between £3,000 and £10,000 are rising by over 100%. For example, a claim for £3,500 will attract an increase from £85 to £180. A claim for £6,000 will attract an increase from £190 to £400.

Charles Wilson, CEO of Lovetts says: “From the outset, the Government has failed to distinguish between the claimants that specialise in consumer collections, or debt purchase, and the heart of UK business which is mid-range bulk debt dealt which will see Court Fees almost double overnight. Essentially, the heartland of commerce will, for at least 50% of its claims from £1500 to £15,000, be paying an increase of 97%.”

Of course, we are actively advising our clients be vigilant in recovering all Late Payment compensation, interest and costs possible, but it is the risk of non-payment that may deter creditors from seeking redress through legal channels. It is the most vulnerable businesses that will not wish to take this risk.

“These proposals therefore make a mockery of the Government’s initiatives to combat late payment – it’s a classic own goal. The very real danger is that businesses will be tempted to just give up and write-off the debt. Poor payers gamble on the reluctance by SMEs in particular to risk court fees on modest claims of up to £10,000. This combined with the fact that most firms set policies based on risk and cost-effectiveness points to a situation where late payers will know they have nothing to fear and the whole system of commercial redress will fall into serious disuse and disrepute.”